I've been scratching my head over Riot Platforms' (NASDAQ: RIOT) stock performance lately. Despite the company showing impressive operational progress, its stock is down over 50% year-to-date (YTD). This puzzling decline calls for a deeper look to find out why.

From their latest 10-Q report and recent presentations, Riot seems to be following a promising trajectory:

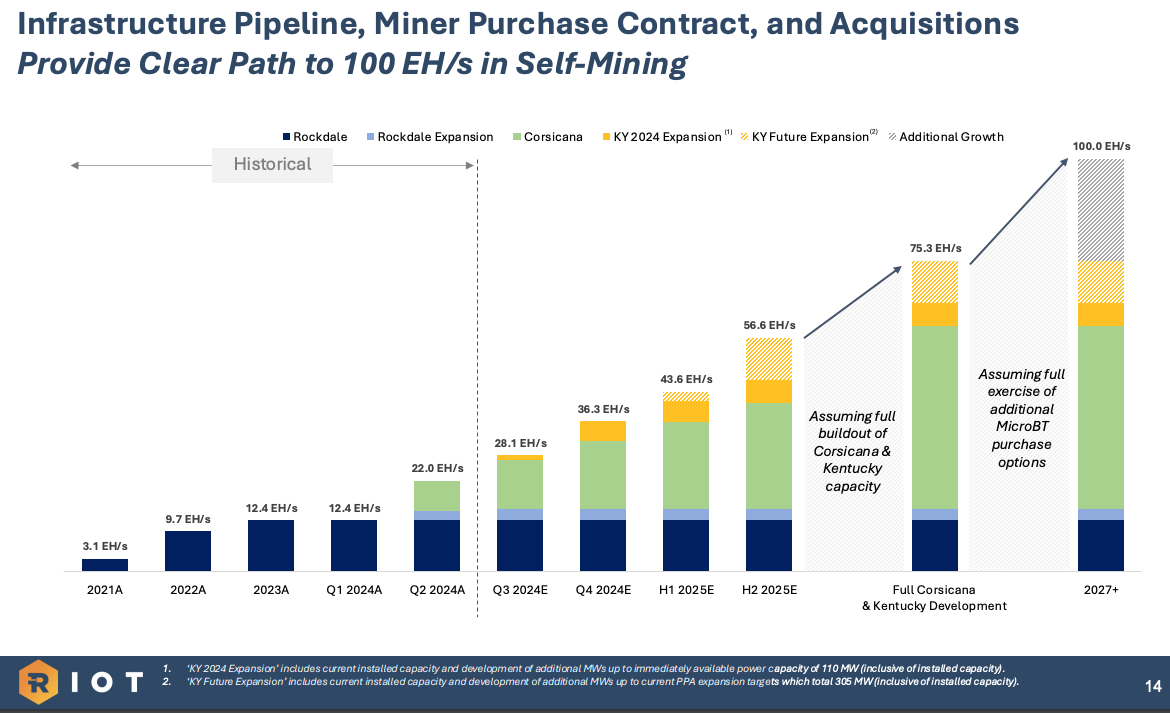

- Rapid Mining Capacity Expansion: They've achieved a remarkable 193% year-over-year growth in hash rate, with solid plans to expand even further by the end of the year and into 2025.

- Competitive Bitcoin Production Costs: Riot has managed to keep their production costs relatively low, which is crucial in the energy-intensive Bitcoin mining industry.

- Zero Long-Term Debt: A debt-free balance sheet provides financial flexibility.

- Substantial Bitcoin Reserves: The company holds 9,334 BTC, valued at approximately $585 million as of June 30, 2024.

- Profitable Power Curtailment Deal: Riot’s agreement with ERCOT has earned them millions in energy credits, further boosting their financial position.

So, why isn't the stock market reflecting this optimism?

Mixed Analyst Ratings and Community Sentiment

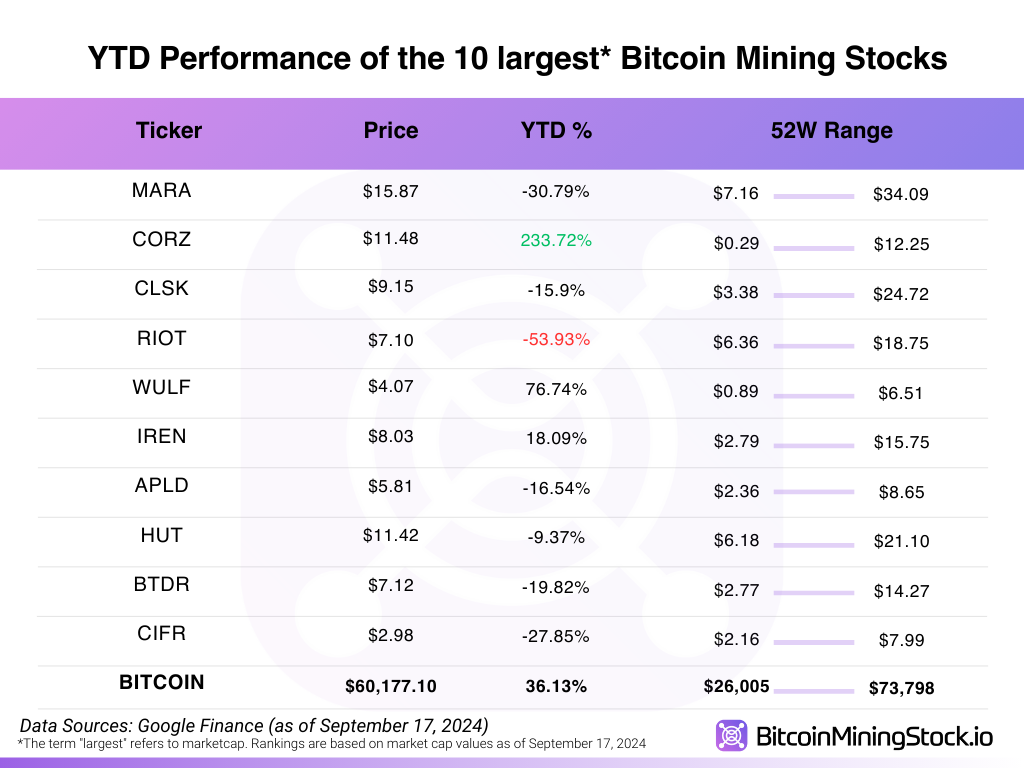

Despite these achievements, analyst ratings on RIOT remain mixed, featuring both bullish and bearish perspectives. Personally, I find community sentiment to be valuable—it often offers quick and unique insights. This year, Riot's stock has lagged behind its peers and even Bitcoin itself. Companies like CleanSpark (CLSK) have overtaken Riot in industry rankings (by market cap).

After digging through community discussions and public data, I've summarized several potential reasons behind Riot’s stock dip.

Industry Challenges and Riot's Strategic Choices

First, we need to consider the broader industry context. The industry itself is facing significant headwinds. The Bitcoin halving and decreasing hash prices are putting pressure on miners. They have limited options: ramp up operations, improve efficiency, or seek alternative revenue streams. While some miners are diversifying into areas like AI (which we've covered in previous analyses), Riot has chosen to double down on Bitcoin mining.

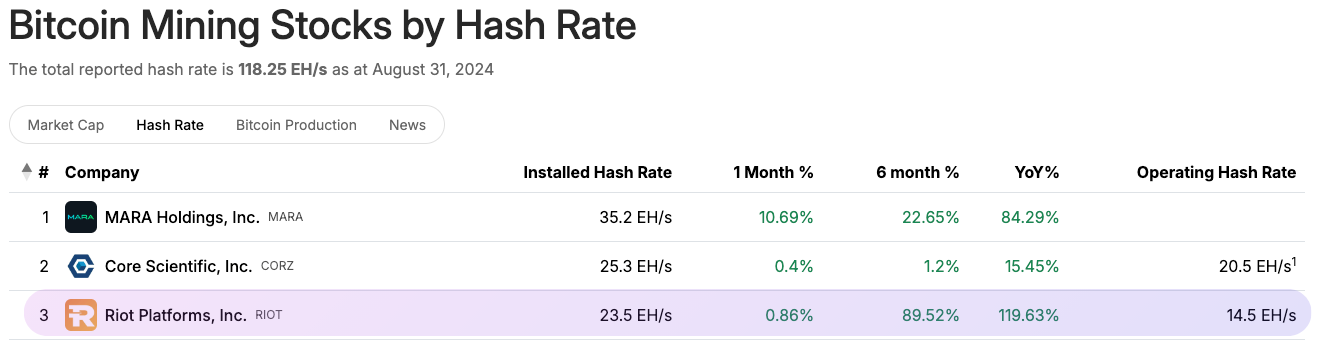

As of August 31, 2024, Riot's hash rate grew by an impressive 119.63% YoY, reaching 23.5 EH/s. This growth keeps Riot among the top 3 miners by hash rate. However, this expansion isn't unique enough to be a standout selling point. Almost all major miners—including Marathon Digital Holdings (MARA), CleanSpark (CLSK), TeraWulf (WULF), Iris Energy (IREN), and Bitfarms (BITF)—have announced ambitious expansion plans for 2024 and 2025.

The core issue boils down to cost and revenue. Simply increasing mining capacity doesn't guarantee profitability, especially when the market is saturated, and Bitcoin prices are volatile.

The Cost and Revenue Conundrum

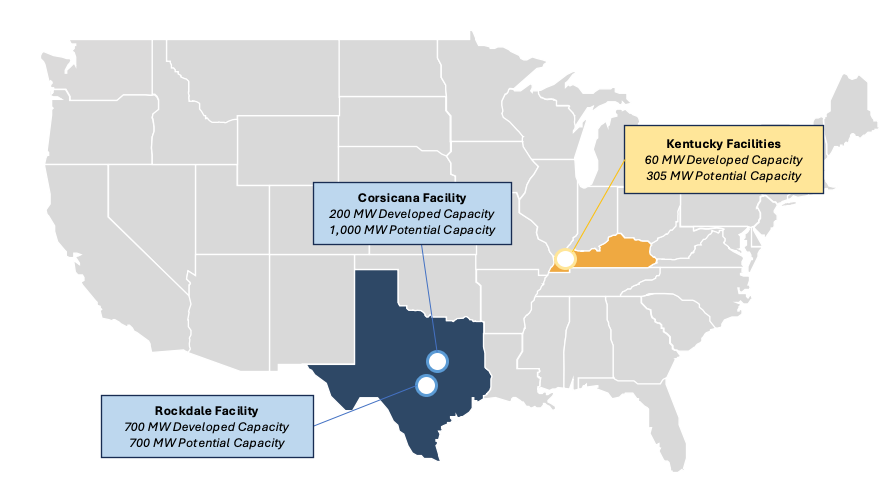

Let's dive into Riot's mining costs. In Q2 2024, their non-GAAP direct cost to mine was $25,327 per Bitcoin, factoring in power curtailment credits. However, under GAAP standard, the cost was significantly higher at $41,795 per Bitcoin. We can expect these costs to increase in the third quarter due to higher electricity expenses in summer months, given that approximately 93.75% of Riot's deployed power capacity is located in Texas—a state known for summer heat waves. Subsequently, potential reductions in mining efficiency can be caused as well.

In the second quarter, Riot reported an adjusted EBITDA loss of $75.2 million, with Bitcoin prices averaging around $66,071. Looking ahead to the third quarter, with Bitcoin prices mostly in the $50,000 to $60,000 range and fewer Bitcoins mined, similar or even greater losses are possible. It's important to note that mining contributed 80% of Riot's revenue in the second quarter, a figure unlikely to change dramatically in the near future.

Once again, I’d like to stress that cost and revenue challenges aren't unique to Riot; they affect the entire mining industry.

Cash Flow Considerations: Was Capital Deployed Effectively?

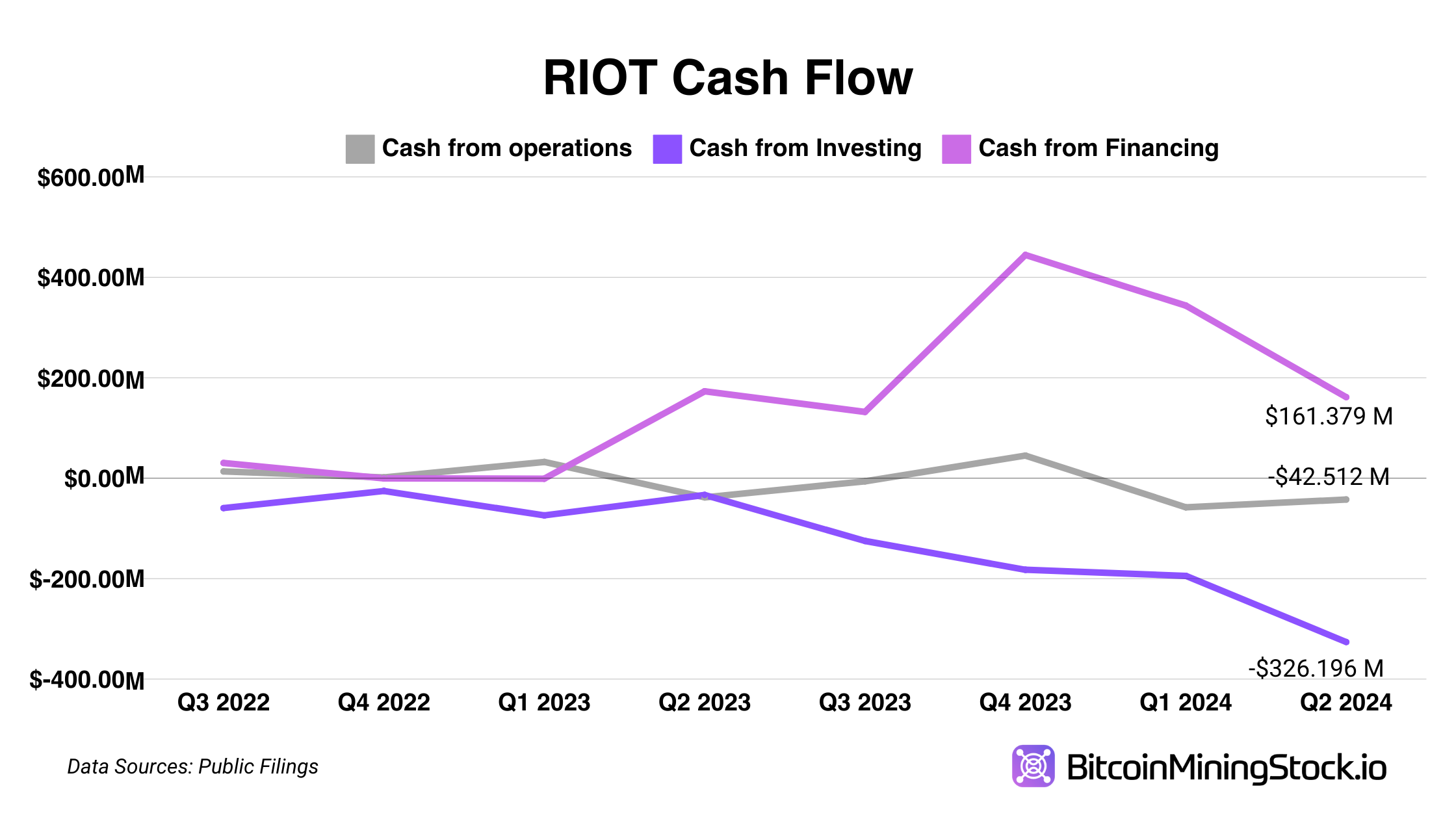

Examining Riot's cash flow provides further insights. As of June 30, 2024, the company's cash and cash equivalents stood at $481.168m, up from $289.276m the previous year. However, their net cash used in operating activities soared to $100.365m from just $5.784m last year. This surge was mainly driven by changes in the fair value of Bitcoin holdings and derivative assets.

Net cash used in investing activities also increased significantly to $520.689m from $107.458m. Major expenditures included deposits on equipment ($278.987m), security deposits ($181m), investments in marketable equity securities ($133.16m), and purchases of property and equipment ($110.848m).

To fund these substantial investments, Riot has been issuing additional shares, leading to significant dilution, which is already weighing on the stock. Over the trailing 12 months, the company has raised over $1b—nearly half of its current market value. In August 2024, Riot filed for a $750m controlled equity offering. Earlier, February 2024, Riot registered a $750m at-the-market (ATM) offering. They also had a $750m ATM offering in 2023 and pursued a $500m ATM offering in 2022.

While financing vehicles like these aren’t inherently negative, especially if it fuels growth and leads to robust cash flows, the key concern is whether this dilution will translate into higher returns for shareholders. Investors might be skeptical about whether these capital raises are being deployed effectively.

The Bitfarms Acquisition Attempt: A Misstep?

Lastly, let’s look at Riot's M&A activity, particularly their attempt to acquire Bitfarms (BITF). It Is widely known that Riot has been facing significant resistance since the start of the execution. On August 13, Riot announced an 18.9% beneficial ownership in Bitfarms, making it one of the largest shareholders, but its takeover efforts have not been well-received.

A public statement from Bitfarms suggests resistance to Riot's plans, casting doubt on the success of this merger attempt. A few weeks ago, Bitfarms announced the acquisition of Stronghold Digital Mining (SDIG) to further fend off Riot's potential M&A plans.

Riot's approach, including the launch of www.ABetterBitfarms.com, has been perceived by some as aggressive and perhaps lacking corporate maturity. Such tactics might have backfired, potentially harming Riot's reputation and undermining investor confidence. Historically, forceful acquisition attempts often don't end well, and this situation might have painted Riot in a negative light.

Additional notes: According to an anonymous industry veteran with over 30 years of M&A experience, Riot Platforms is facing increased costs in its attempt to acquire Bitfarms due to the latter's resistance. While I am not an expert on the subject, the following is a compilation of insights provided by this experienced individual. For those interested in a deeper understanding, you can refer to the original articles for more detailed information.

Riot Platforms' attempt to acquire Bitfarms faces significant cost hurdles due to defensive measures enacted by Bitfarms under Canadian takeover laws; unlike U.S. "poison pill" strategies that can be legally challenged, Canadian regulations allow companies to adopt such defenses during an active takeover, deeming any acquisition exceeding a 15% stake without a formal offer as coercive and unlawful—this plan cannot be overturned for 6 months unless more than 50% of shareholders vote against it, forcing Riot to initiate a formal bid open to all shareholders for at least 105 days and agree to purchase at least 50% plus one share at a fair price, likely needing to offer at least $5 per share (significantly higher than the $2.30 per share previously paid), meaning that after already investing a little over $200m for 19.9% of outstanding, Riot would need to spend additional $500m or more to gain control, dramatically increasing the takeover cost and providing Bitfarms' management with time to seek better deals or alternative strategies, thereby making Riot's acquisition attempt considerably more expensive and complex.

So, What's Next for Riot?

Riot is still positioning itself well for further growth in Bitcoin mining. However, to achieve its vision of becoming the "world's leading Bitcoin-driven infrastructure platform," they'll need to address several key challenges:

- Find a path for long-term profitability: Riot needs to make strategic plans to sustain profitability amid declining hash prices and rising production costs.

- Capital Allocation Discipline: The company should manage its capital expenditures prudently and communicate how these investments will generate shareholder value without excessive dilution.

- Strategic Positioning: Riot may benefit from diversifying its revenue streams or exploring strategic partnerships to mitigate risks associated with a singular focus on Bitcoin mining.

Final Thoughts

The challenges discussed in this analysis are universally applicable to almost all Bitcoin miners. While Bitcoin mining is often considered antifragile—with the belief that there will always be miners securing the network—the reality is that miners need to develop more sophisticated strategies to stay competitive. This means rethinking their business models, optimizing operational efficiencies, and making the best use of financial instruments to drive growth. Only by adopting these refined approaches will mining businesses become truly appealing to investors in the capital markets.

Disclaimer: The views expressed in this article are my own and are based on publicly available information. This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results. No recommendation or advice is being provided as to the suitability of any investment for any particular investor.