If you've been following Bitcoin mining stocks for a while, you'll probably notice: companies tend to issue more shares when they need cash, and your slice shrinks. For years, the pattern almost becomes the norm: dilute the holders and move on.

That's what made IREN's latest financing move stand out to me. The company, which now positions itself as an AI cloud provider more than a Bitcoin miner, just raised $3.65 billion in debt at an investment-grade rating, without issuing a single new share. I had to read the terms twice. The how is more interesting than the headline, and it tells you a lot about which of these companies are actually worth owning.

What IREN actually did

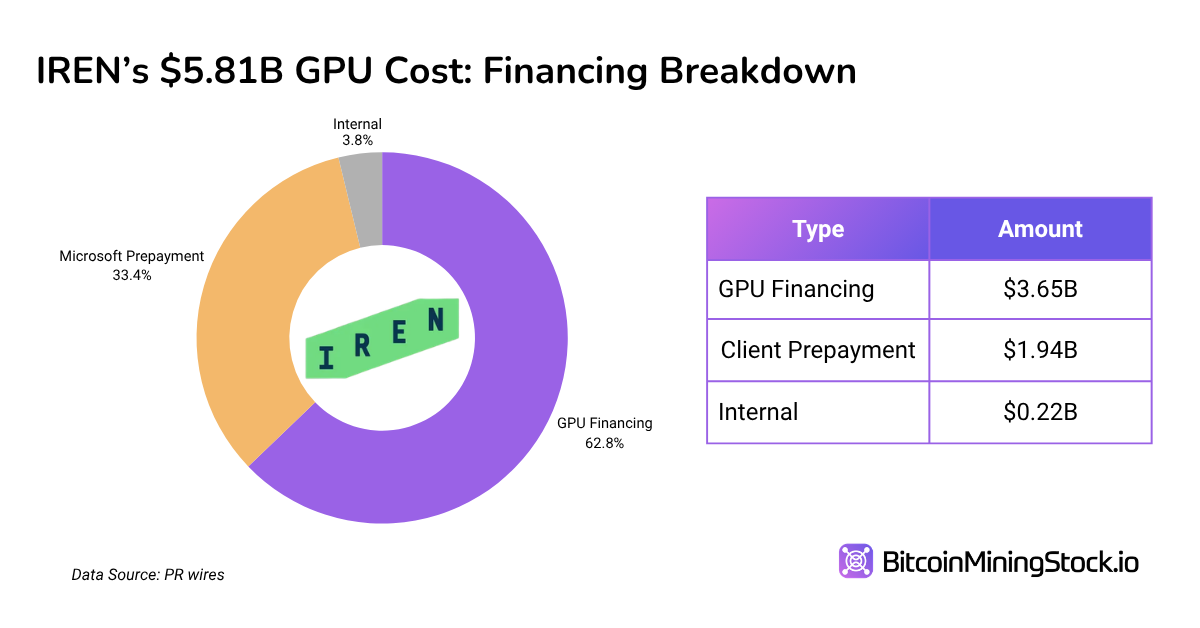

On June 1, IREN (NASDAQ: IREN) closed a $3.65B facility to buy the GPUs for its AI cloud contract with Microsoft. The terms are interesting: a blended cost of 6.00%, arranged by Goldman Sachs and J.P. Morgan, secured against the GPUs and the cash Microsoft is contracted to pay.

Then it gets even better for IREN. Microsoft also prepaid $1.94B of the bill. Between the loan and that prepayment, the company covered about 96% of its $5.81B GPU cost without dipping into its own pocket, all to serve a contract worth $9.7B over five years.

Management says it "essentially got the GPUs for next to nothing" and quotes an all-in cost of 3.31%, though I'd read that number with some caution. It treats Microsoft's prepayment as free money, when a prepayment is really an advance IREN repays later in compute. The honest borrowing cost is the 6.00%. Which raises the real question: how does a company like this borrow billions at 6%, when the sector spent years shut out of the debt markets entirely? The answer is the credit rating.

How the deal earned an investment-grade rating

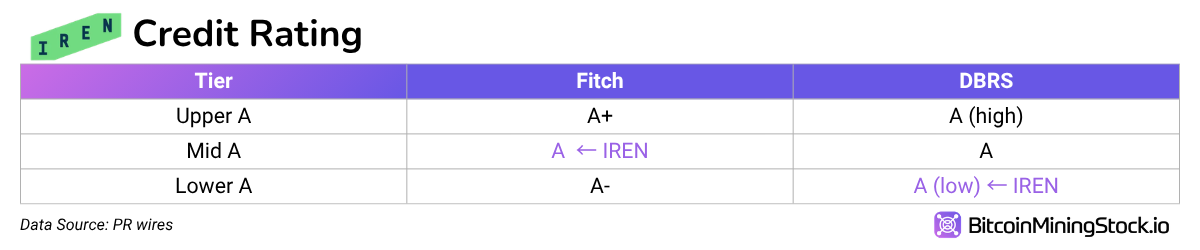

The facility was rated A by Fitch and A (low) by DBRS. A credit rating is simply a grade for how likely a borrower is to repay, and each agency uses its own labels. Here's how the "A" band lines up:

Anything at BBB (Upper B) or above is investment grade. Below that line, debt is considered high-yield, or speculative grade. The A band sits well inside the investment-grade zone.

Now the part that matters. IREN, on its own as a growth company, is nowhere near an A. But the lenders aren't really betting on IREN. They're betting on Microsoft who holds AAA long-term credit rating from the major rating agencies. That is about as safe as a borrower gets. Because the debt is secured by Microsoft's contracted payments, the agencies looked past IREN and the fast-aging chips and graded the strength of Microsoft's promise instead. Strip it down, and IREN borrowed against Microsoft's balance sheet.

That single notch below perfect, an A instead of Microsoft's AAA, is the agencies' price for what Microsoft's promise doesn't cover: GPUs that lose value quickly, and the chance IREN stumbles on delivery.

Why that rating unlocks the cheapest money

An investment-grade stamp doesn't just look good. It decides who is allowed to lend. The market IREN tapped is where insurers and pension funds put their money. They hold huge long-term pools against future claims and payouts, they want steady low-risk income, and the rules largely forbid them from holding anything below investment grade.

Clear the investment-grade bar and you open that door, to the deepest and cheapest capital available. Miss it, and you're left with private-credit funds charging nearly double digits, which is where the sector sat a year ago. The rating is the door. Microsoft's credit is the key.

IREN isn't the first

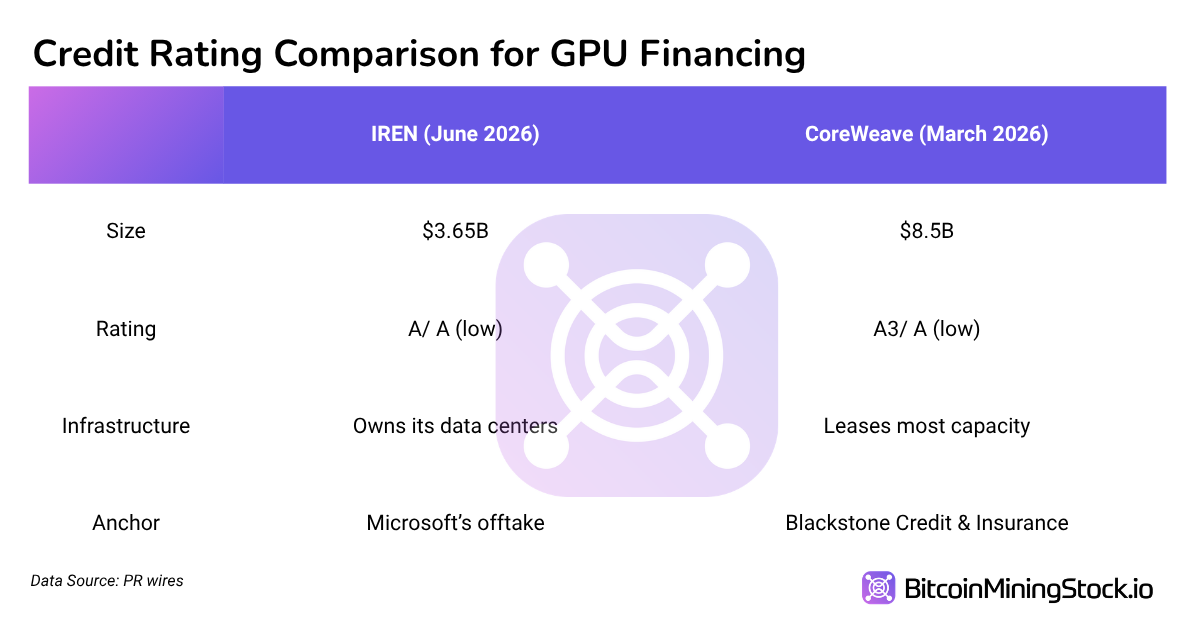

CoreWeave got investment-grade GPU financing in March, closing an $8.5B GPU-backed deal at a nearly identical rating.

IREN's rating is a notch higher, and it owns its data centers while CoreWeave mostly rents. You'd expect that to translate into cheaper money. It didn't. Both priced at almost the same spread, around SOFR plus 2.13% (SOFR is the going benchmark rate). The rating edge and the owned buildings were nice to have. What actually got both deals done was the same thing: a customer creditworthy enough to rate. That's the gate. Everything else is a tiebreaker.

Final thoughts

So what should an IREN shareholder take away from all this?

The upside is real. Funding a $5.81B buildout with debt and a customer's cash, rather than printing new shares, is the reverse of the sector's usual playbook. No dilution, and capital cheaper than the company could find elsewhere.

The catch is leverage. Equity holders now stand behind these lenders, who hold first claim on the GPUs and the Microsoft payments. If that contract underperforms, the debt gets repaid before shareholders see a cent.

Then zoom out, because the rule this sets is bigger than IREN. What now decides which of these companies can fund themselves cheaply isn't their megawatts portfolio. It's whether they've signed a customer whose credit can carry a rating. Both TeraWulf and Cipher have Google-backed Fluidstack (Cipher also has AWS); Applied Digital, Core Scientific, and Hut 8 are chasing the same prize. Land an investment-grade anchor, and you can borrow like IREN. Fail to, and you keep selling shares to survive.

However, I'd still stay a little skeptical. These GPUs age out in three to five years while the debt runs longer, so the agencies are betting the contracts outlast the hardware. And much of this demand is hyperscalers funding the very capacity they plan to rent. So far, it's working. But the question worth asking before buying any of these names is the one IREN just answered for itself: who's their customer, and how good is their credit?

Disclaimer: The views expressed in this article are my own and are based on publicly available information. This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results. No recommendation or advice is being provided as to the suitability of any investment for any particular investor.