(The following is extracted from the chapter Public Miners Diversification in Compute in the Bitcoin Mining Market Review (2025–2026 edition). The report was produced in collaboration with Digital Mining Solutions and is supported by NiceHash 💜)

Over the past few weeks, we've pointed out a clear shift in how capital markets evaluated public Bitcoin miners in 2025. From the second half of the year onward, investors increasingly favored companies with credible HPC/AI exposure.

This wasn’t a sentiment-driven trade. It coincided with a sharp acceleration in execution. In 2024 only one public miner, Core Scientific, had secured a hyperscaler agreement. In 2025, that number rose to five. What was once framed as experimental diversification is now shaping balance sheets, development pipelines, and long-term strategy across the sector.

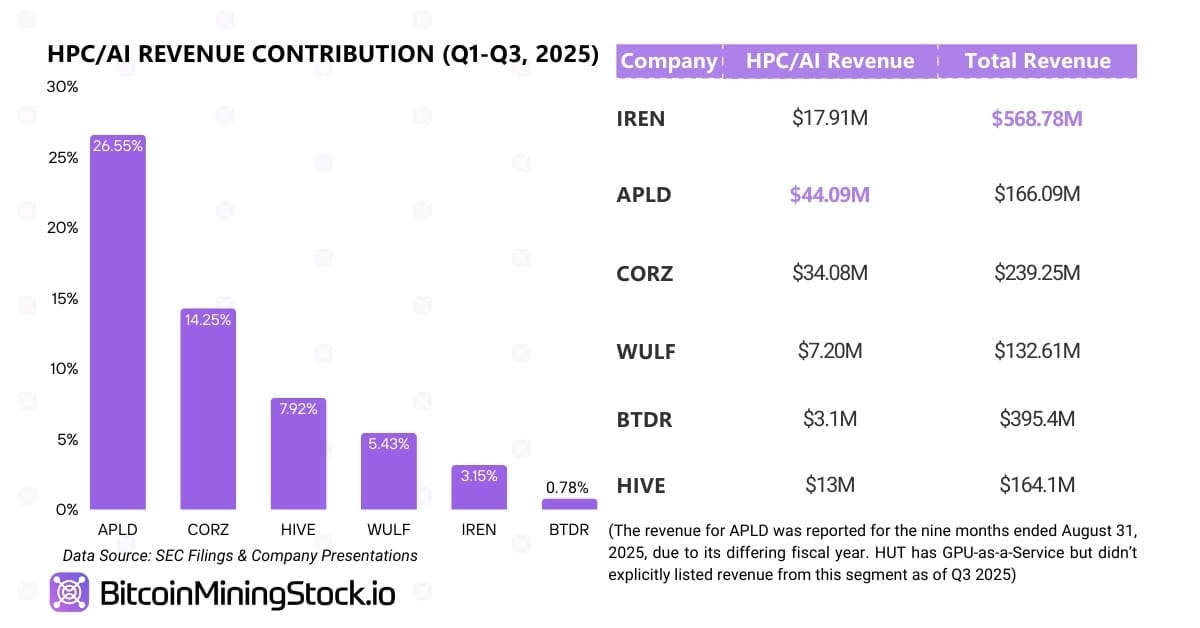

Revenue Is Still Small, But Revenue Visibility Improves

Despite the surge in announcements, HPC/AI revenue contribution remained limited through 2025, which is expected. Most hyperscaler deals are structured as long-term contracts with phased infrastructure rollout. Capacity is being built and energized in stages, with meaningful revenue expected to ramp beginning in 2026 and beyond.

Not All Hyperscaler Deals Are the Same

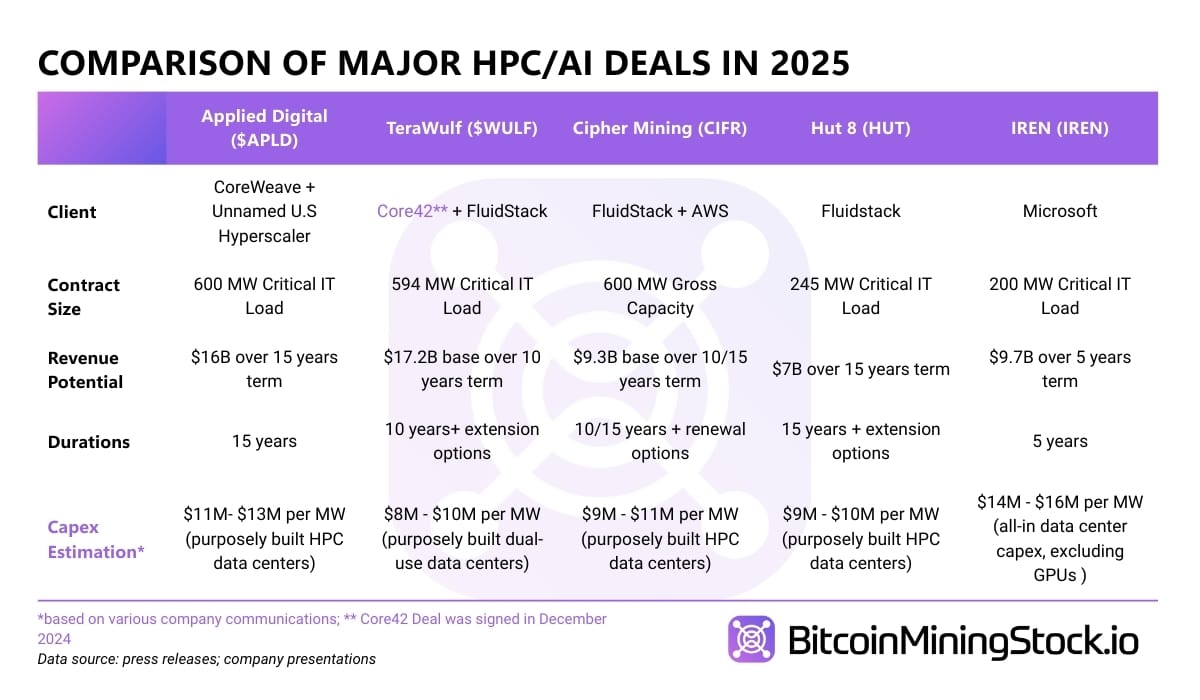

While all announced deals have hyperscaler exposure, the underlying business models differ significantly. In most case, miners are positioning themselves as HPC infrastructure providers rather than AI cloud operators. Their role is primarily colocation: delivering power, cooling, and physical infrastructure, not selling AI cloud directly.

The distinction matters, because Capex, margins, execution requirements vary. Two contracts with similar headline values can produce very different economic outcomes depending on whether the miner is operating GPUs or simply hosting them.

*Refer to the original report to get full details on deals breakdown, data center locations and more for each individual company.

For Some Miners, This Isn’t Diversification Anymore

The more interesting shift is happening underneath the headlines. For several companies, HPC is no longer a side business. It’s where future capital is going.

Some miners will continue running Bitcoin fleets as long as they remain profitable. But their development pipelines are now almost entirely HPC-focused, such as IREN and TeraWulf. Companies like Bitfarms have gone further, signaling that Bitcoin mining itself may be wound down over time.

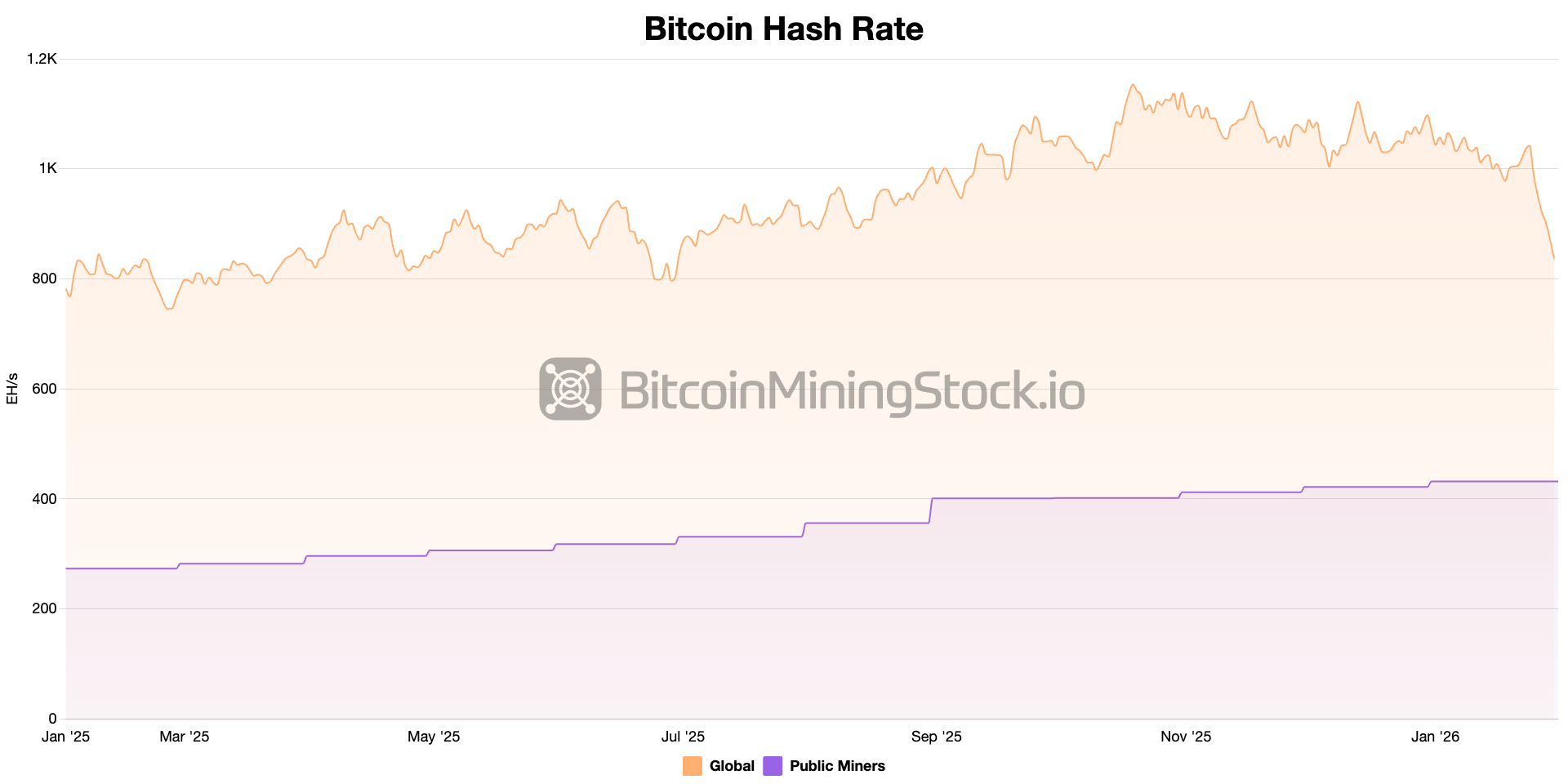

This shift has second-order effects. If public miners increasingly allocate capital and power capacity toward AI/HPC workloads, aggregate hash rate growth from public companies is likely to slow, flatten, or even decline.

Pivots Are Not Feasible For Everybody

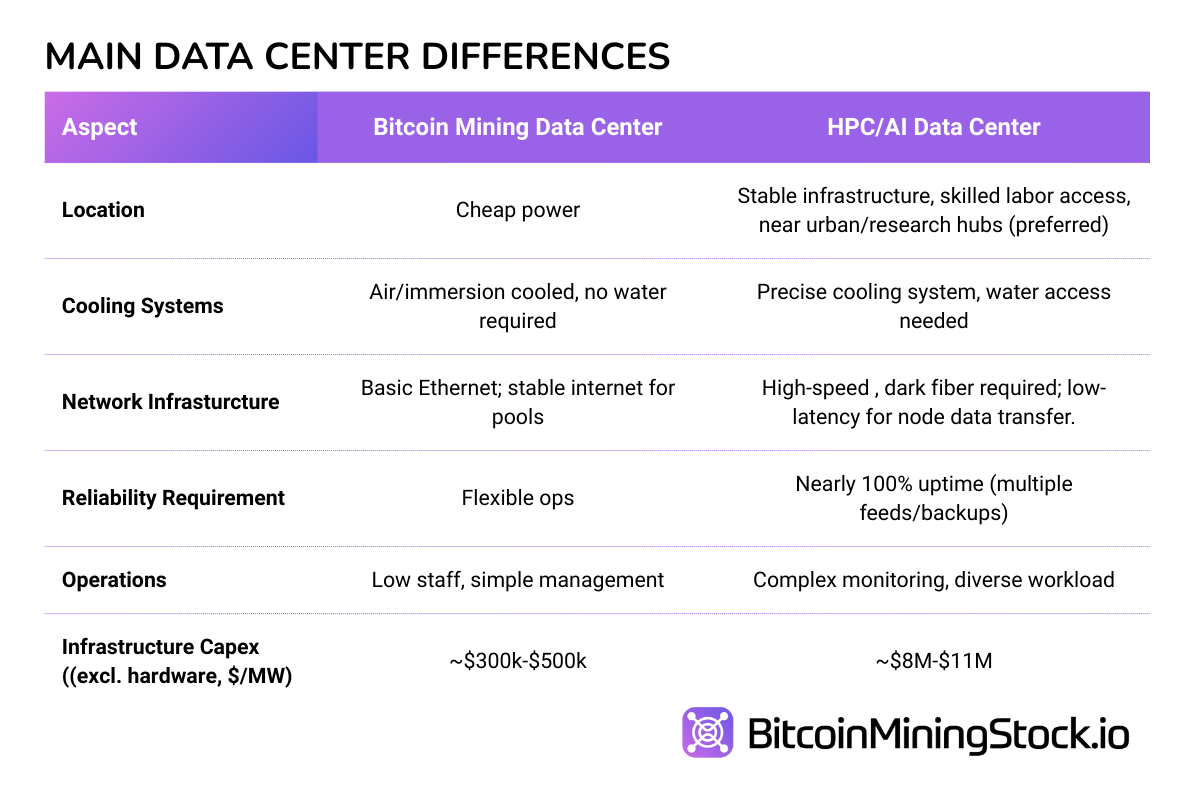

HPC/AI pivots may be discussed, but it will be wrong to assume that transitioning is broadly available to anyone with power and land. In practice, most mining sites were designed for speed and flexibility (mining containers are widely used), not for the density, redundancy, and operational discipline hyperscale workloads require. Some sites can be adapted, for example, Core Scientific is modifying (~$1.5-3M per MW) their existing Bitcoin mining data centers to fulfill contracts with CoreWeave. Many cannot, or only at a cost that erodes the economics of the pivot.

Capital and execution are the real constraints. HPC buildouts require large upfront investment ($8-11M per MW vs $300-500K per MW) and different operating expertises. Even with the right infrastructure and technical capabilities, monetizing a HPC operation takes time and unlike Bitcoin mining there are no guaranteed block rewards to fall back on.

One Prediction: More Deals, Less Narrative

Hyperscaler announcements are likely to continue into 2026, given miners already control what AI buyers need most: permitted land, power access, and development capability.

But the market is changing how it reacts. Megawatt counts and headline contract values are no longer enough. Investors are asking harder questions: who funds the build; when revenue actually starts; what happens if the customer walks; whether risk truly sits at the project level or quietly flows back to the parent company...

Essentially, not every HPC deal will re-rate a stock the same way. The premium will increasingly go to structures that de-risk the business model and to operators that can execute without stacking expensive capital on top of already cyclical mining cash flows.

After the HPC Pivot: What’s Next for Bitcoin Mining?

(The following perspective was not included in the original report, but it’s worth sharing here, as many readers have raised the same question.)

For some, the growing shift of public miners toward AI and HPC infrastructure is seen as a threat to Bitcoin mining. In reality, it might be the beginning of mining’s evolution. As capital, expertise, and energy capacity flow toward high-value AI workloads, the landscape of Bitcoin mining is starting to look different. When larger miners scale back or exit Bitcoin mining, their former capacity, hardware, and resources will redistribute across new geographies and business models.

One visible effect will be a shift in where mining happens. While AI data centers compete for the best power sites in mature markets, especially in North America, Bitcoin miners will be pushed to places with stranded energy, flared gas, and smaller or off-grid power sources. These environments favor flexibility over scale. A mining load that once sat on a hyperscale campus in Texas may reappear as a set of modular containers in Paraguay, Ethiopia, or Scandinavia, in which fleets still contribute to network security, but with very different economics and risk profiles.

At the same time, mining will evolve how it operates. Unlike AI workloads, Bitcoin mining doesn’t require constant uptime or redundancy. That makes it ideal for hybrid setups where mining serves as a buffer that absorbs excess power, participates in demand response programs, and lowers overall energy costs. In these environments, mining isn’t the primary product but a valuable tool in integrated energy infrastructure.

This evolution will also likely to raise the bar for miners who remain focused on Bitcoin. The old model: buy ASICs, plug into cheap power, and wait - will become harder to sustain. In a more competitive landscape, operators may need to offer grid services, reuse heat, or build closer ties to power suppliers, so that they can generate multiple revenue streams.

None of these are guaranteed outcomes. But one thing is certain - Bitcoin mining will continue to evolve.

📙 Note: This article is intentionally skipping details. If you want to go deeper into individual companies and their contract structures, delivery timelines, capital intensity, and more, please refer to the original report.

Disclaimer: This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results. No recommendation or advice is being provided as to the suitability of any investment for any particular investor.