I was not aware of Situational Awareness LP until recently. Earlier last week, CleanSpark rallied while majority of bitcoin-mining peers were trading in the red. The speculation on X attributed the move to Leopold Aschenbrenner increasing his position significantly in the latest 13F. That got me curious enough to read the filing properly. What I found turned out to be more interesting than the CleanSpark speculation.

Who Leopold Aschenbrenner is, and what Situational Awareness is

When Leopold Aschenbrenner published Situational Awareness in mid-2024. The 165-page essay argued that artificial general intelligence was much closer than the public consensus believed, that compute and power infrastructure would be the binding constraint, and that the buildout to support it would be the defining investment story of the late 2020s.

He launched a hedge fund of the same name shortly after. Six 13F filings later, Situational Awareness LP is read religiously by a meaningful slice of AI investors. The fund gets called the Cathie Wood of AI infrastructure, though the track record is short, just six quarters, and it has never been tested in a real drawdown.

Should you copy his trades? That is a good question. Let's take a close look.

Six quarters of growth

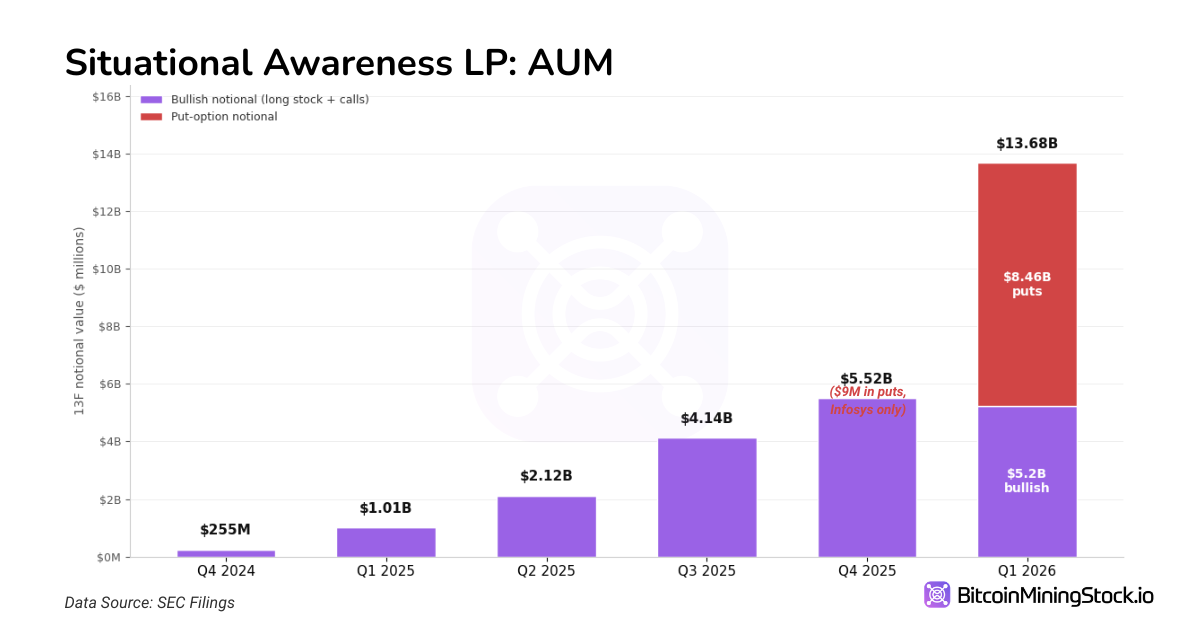

Situational Awareness LP first appeared on the 13F radar in late 2024 with a small $255M book. It has grown almost every quarter since.

The fund crossed $1B in Q1 2025 and $5B in Q4 2025. Q1 2026 is the biggest jump yet, more than doubling to $13.7B. But the long stock plus call portion of the book barely moved (from $5.5B to $5.2B). The entire growth in reported 13F notional is a brand new $8.5B put-option book on the semiconductor complex. Notably, five previous quarters Aschenbrenner had no meaningful put exposure at all (just a $9M Infosys put in Q4 2025). Q1 2026 is the first time he is filing a real options book.

What the Q1 2026 book actually looks like

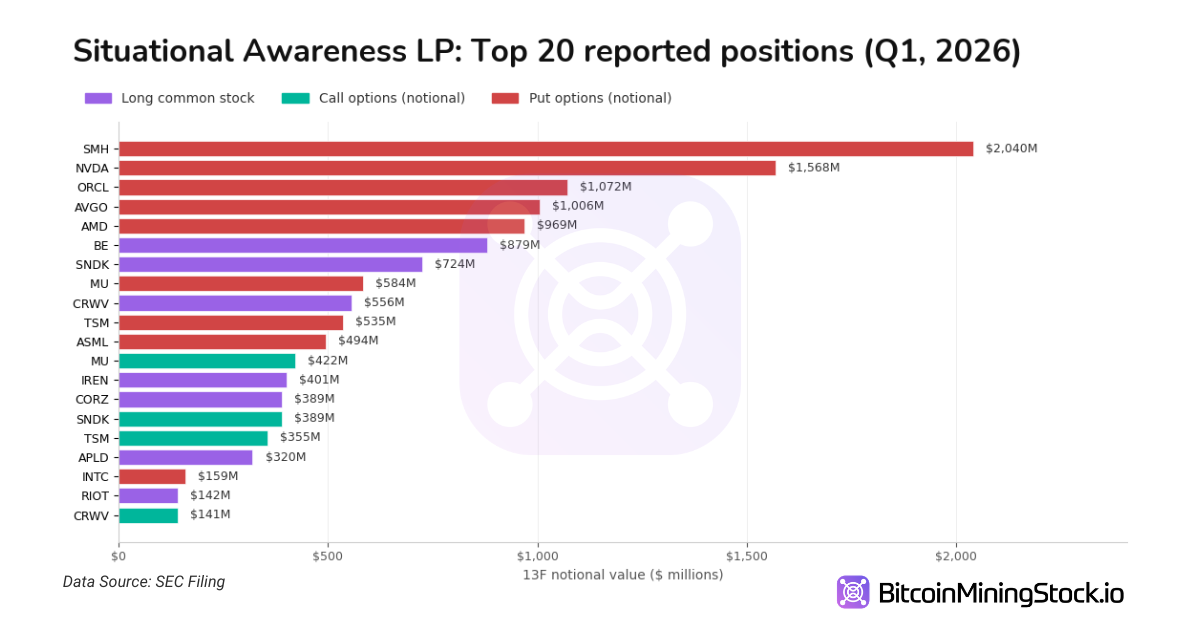

Here are the largest reported positions, color-coded by type. Blue is long common stock, green is call options, red is put options.

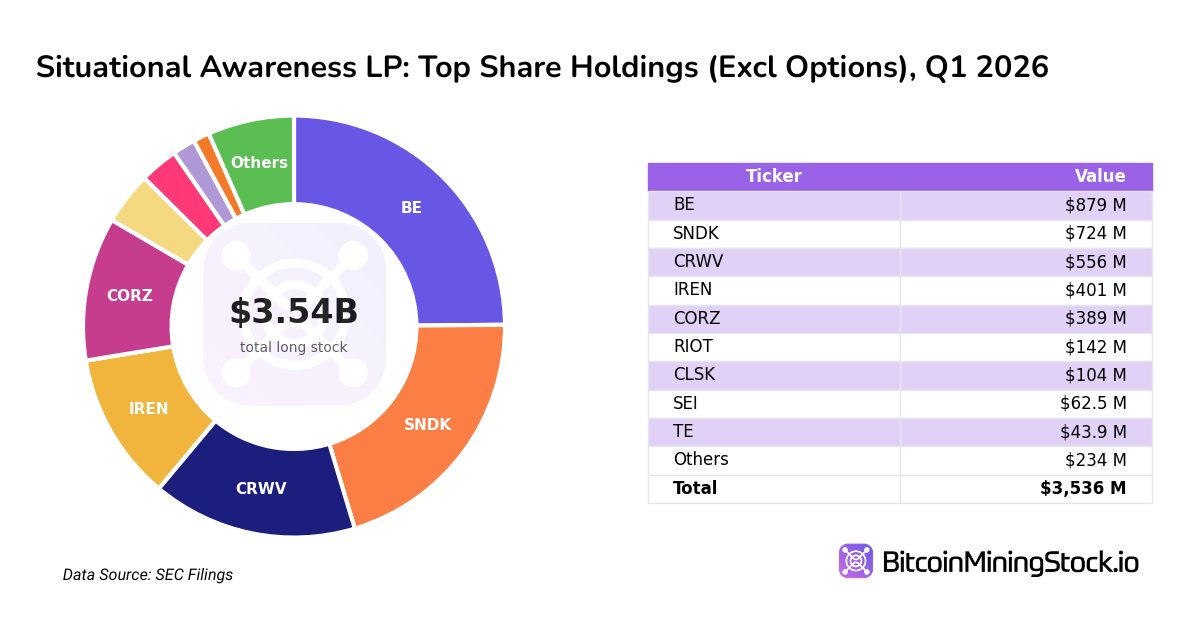

The single biggest line in the entire fund is no longer a stock pick, it is a $2.04B put on the VanEck Semi ETF (SMH). Five of the next six lines are also puts (NVDA, ORCL, AVGO, AMD, MU). The largest bullish position is Bloom Energy at $879M of common stock, with CoreWeave and SanDisk close behind.

A few details to flag. NVDA is a brand new position- $1.57B put on 8.99 million shares with no offsetting long. Oracle, Broadcom, AMD, and ASML are also fresh puts of roughly $0.5B to $1B each. Micron and Taiwan Semi carry three-legged structures (put, call, and a small long on the same name), which looks less directional and more like long-volatility positioning. Intel went the other way: Q4 held a $747M bullish call on 20 million shares, Q1 holds a $159M put and a 202K-share residual long. Same name, opposite position, in a quarter's time.

Reading the put overlay

This is the part of the filing that deserves the most attention, because the natural reading could be Aschenbrenner turned bearish on the AI semi complex. Is that the case though?

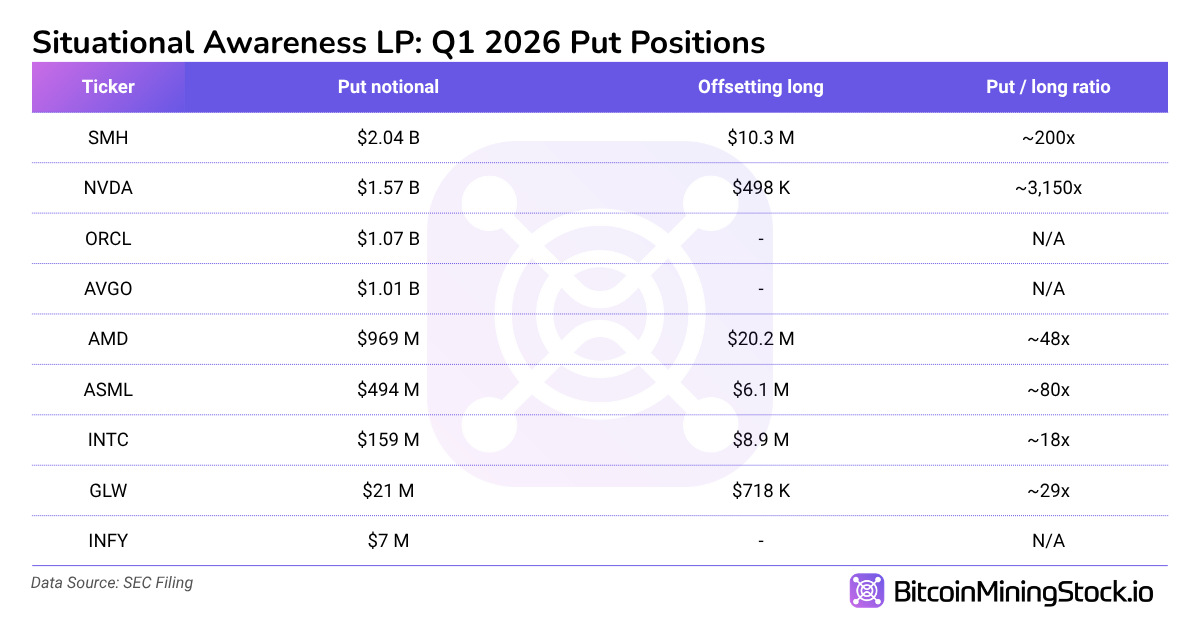

There are eleven names where the fund owns puts. On nine of them, the put exposure dwarfs any offsetting long position by anywhere from ~18x to ~3,150x .

If those puts are standalone bought puts, the bearish read is probably right. But the 13F can't confirm it. Many details like whether the puts are bought or sold, or what strikes and expirations are involved are missing in the filing. Any of those changes the read materially. As a result, bearish could be a strong possibility, but not a confirmed call.

Micron and Taiwan Semi are the outliers. Both carry roughly matched puts and calls alongside a small long, which looks more like long-volatility positioning than a directional view.

Intel, on the other hand, is the cleanest reversal in the filing. Q4 held a $747M call on 20.24M INTC shares; Q1 holds a $159M put plus a 202K-share long stub. The structure of the book around Intel has clearly flipped, even if the directional intent of the new put line is open.

Anyway, a reminder before we move on: 13F reports options at notional value of the underlying shares, not premium paid. The actual cash outlay on the $8.5B put book should be much smaller.

Where the conviction shows up

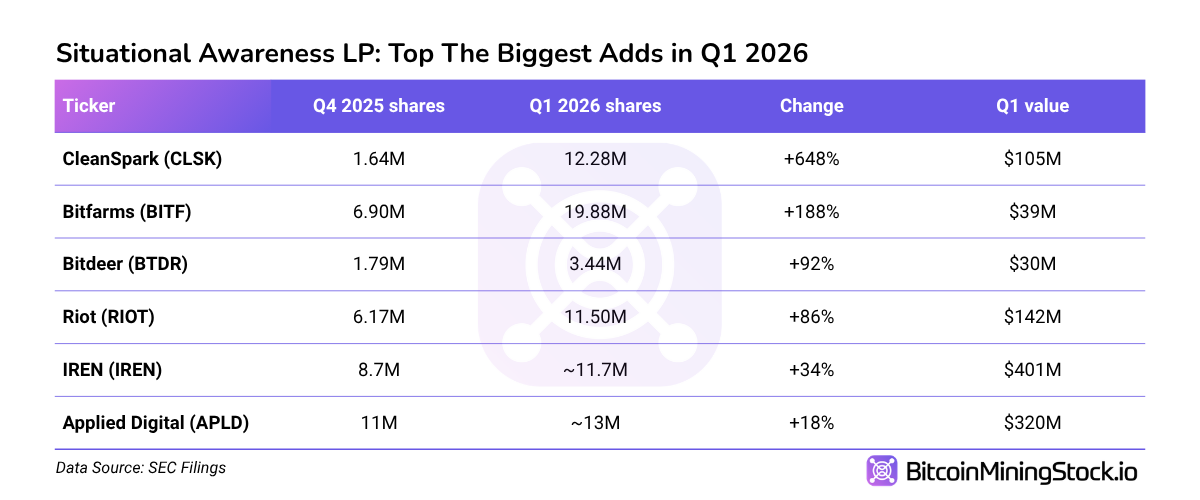

The other side of the filing, the position adds, is where the bullish thesis still speaks clearly. The bitcoin miners are where Aschenbrenner leaned in hardest, and the ranking of the increases is informative on its own.

The bigger percentage adds sit at the smaller-cap miners, while the larger names that already carried the HPC-pivot premium (IREN, Applied Digital) got smaller but still got meaningful adds. That pattern is consistent with a catch-up read, where the cheaper miners close some of the valuation gap to the names already trading on AI-data-center expectations. It is not a wholesale rotation, the larger names were not trimmed to fund the smaller ones, but it is a clear vote that the AI-power and HPC-hosting story is broader than the four or five names retail tends to focus on.

Three brand new long positions point in the same direction: T1 Energy ($44M, a US solar and battery integrator), SharonAI ($18M, Neocloud provider), and HIVE Digital ($6M). Small in absolute dollars, but each fits a broader AI data center and power theme rather than a one-off bet.

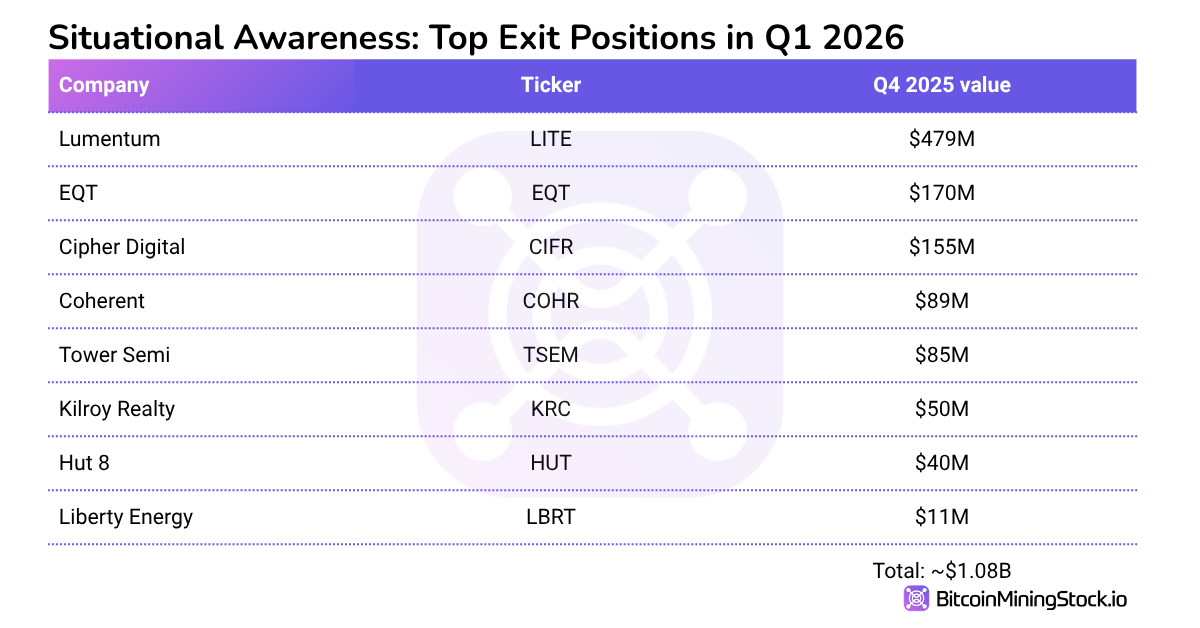

What got cut

Eight names left the book entirely between Q4 and Q1. And there is no single clear pattern of the companies got cut. As a result, any read on motive here is speculative.

However, the eight exits freed up ~$1.1B of capital, which could have been used to fund some of new positions.

Final thoughts

My honest read of this filing is two-part. Aschenbrenner is still long the AI infrastructure: Bloom Energy, SanDisk, CoreWeave, IREN, Core Scientific on the existing book, plus meaningfully larger crypto-miner positions (CleanSpark up 7x, Bitfarms up nearly 3x, Riot and Bitdeer both close to doubled), and three brand new long lines in T1 Energy, SharonAI, and HIVE Digital. The bullish thesis on power, data centers, and HPC-pivot miners is alive and arguably stronger than it was in Q4.

At the same time, the fund has built a large put-option book with the SMH ETF, Nvidia, Oracle and Broadcom as the largest expressions. The puts dwarf any offsetting longs on those names. This can be easily read as Aschenbrenner is bearish on the AI semi complex. However, the 13F does not actually confirm directional intent. The filing does not disclose short puts, or what strikes and expirations are involved. A confident bearish read requires more information than the 13F alone provides.

For an everyday investor, the practical takeaway is two-sided. The bullish position adds (the smaller-cap miner moves, the new long lines, the maintained core longs) carry clear and mirror-able signal. The put book carries a signal too, but a softer one: Aschenbrenner has now built a large enough options position on the chip side of the trade that it materially shapes the risk profile of his book. Treat it as a flag worth watching rather than a confirmed view, and certainly not a short-NVDA recommendation.

With that all said, it's worth mentioning that the current 13F is dated March 31, so positions may have moved since. The next 13F (due mid-August) will tell us whether the put book grows, shrinks, or rotates. That filing will tell us more clues on Leopold Aschenbrenner's updated thesis.

Disclaimer: This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results. No recommendation or advice is being provided as to the suitability of any investment for any particular investor.