Some investors believe in Bitcoin's long-term value and want that exposure inside a regulated structure. Their options have all gotten worse. Self-hosting is operationally complicated, and reliable hosting providers are hard to find. The mining equities used to be the cleanest proxy but the link has broken. The top performers of 2025, $IREN, $APLD, $CIFR, priced like AI infrastructure stories, not Bitcoin producers. In general, ticker selection has gotten harder, and shareholder value keeps eroding through dilution.

The Omnes Mining Note (OMN) is the first product I’ve seen that closes that gap. Basically, its pitch is simple: You get exposure to the hash rate, not to the mining company.

A simple version

Holding a public miner stock is like buying a whole chocolate factory. You get a slice of the chocolate. You also inherit the factory. The owner might decide to make gummy bears instead. The power bill might double. Someone might print more shares of the factory while you’re sleeping, and your slice gets smaller.

OMN is the other version. Imagine a group of chocolate factories agree to pool every bar they make into one locked box. You buy a slip of paper that says: this much of what’s in the box belongs to you. A neutral guard holds the only key. Not anyone who works at the factories. If a factory shuts down, your chocolate is still in the box. If all the owners run off to the Bahamas, the guard still has to hand you your share.

That’s OMN, with Bitcoin instead of chocolate.

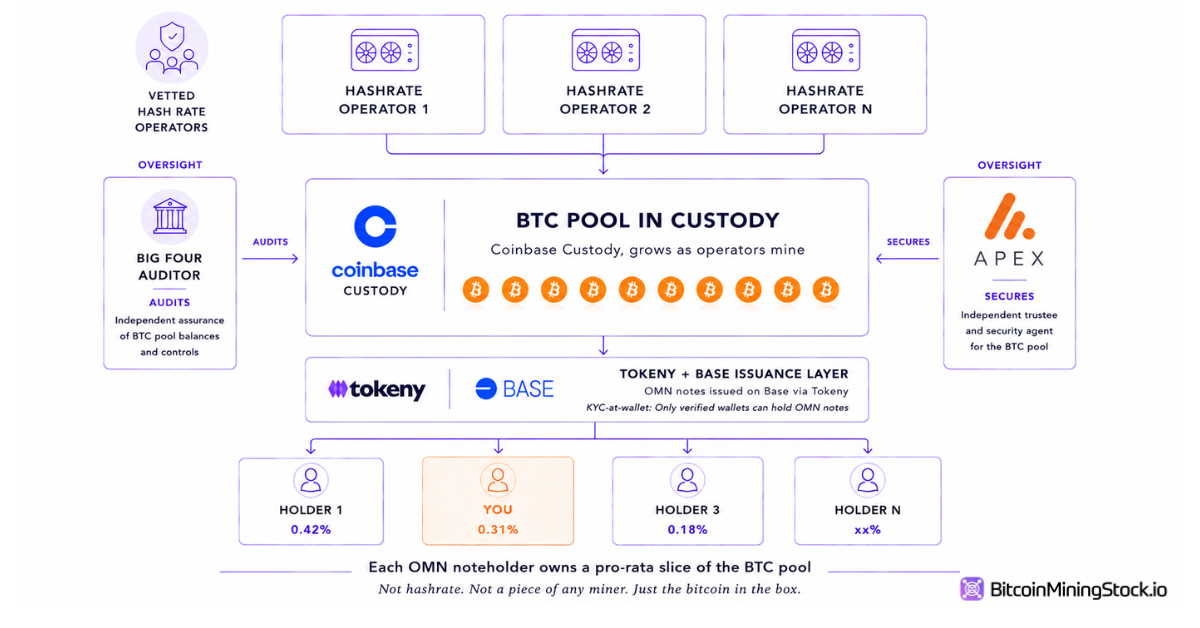

So what does a holder actually own?

Not hash rate. Not a piece of any miner. Not a stream of mining contracts.

A holder owns a Bitcoin-denominated secured hashrate-backed note. It’s a claim on a pool of Bitcoin held in a third-party qualified custody account, secured by an independent security agent. The Bitcoin in that pool is produced as the hash rate backing the notes continuously mines Bitcoin. As mining progresses throughout the tenor of the note, the Bitcoin pool keeps growing. The notes value moves with the Bitcoin pool.

So your exposure is to Bitcoin accumulation from a diversified hash rate base, not to any single Bitcoin mining operator’s share price, ATM cadence, or strategic pivot. If a miner in the pool produces less, the pool grows more slowly. If the hash rate goes up and a miner produces more, the pool grows faster. You’re long the output, not the company.

Yield mechanics, redemption windows, and how returns are paid out live in the offering documents. Read them before any actions. The point worth holding onto is this: What you own is denominated in Bitcoin, secured by Bitcoin, and tracks Bitcoin.

The actual version

The factories are a portfolio of vetted institutional hash rate operators. The locked box is Coinbase Custody. The neutral guard is Apex Corporate Trustees, acting as independent security agent on behalf of noteholders. Apex Group administers the fund. A Big Four firm audits it. The slip of paper is a permissioned token issued on Base via Tokeny, with KYC and eligibility enforced at the wallet level rather than bolted on after.

None of those names are crypto-native experiments. They’re the same ones institutional allocators already use for spot BTC.

What changes for the holder

OMN holders sit in a secured position against pooled hash rate output. There’s no share count to dilute, no management team deciding to pivot into AI hosting, no quarterly equity story to defend. The trustee structure means if something goes wrong at the issuer, you’re not last in line.

That’s a meaningful change from holding miner equity, where capital structure risk and operating risk get bundled into a single ticker.

What it doesn’t do

OMN is not a substitute for miner equity if what you actually want is operational leverage. You don’t get the upside of $IREN turning into a credible AI compute story. You don’t get the multiple expansion when a sub-scale miner gets re-rated. You don’t get the optionality on a treasury strategy.

Final Thoughts

OMN isn’t a replacement for miner equity. It’s a different sleeve. If your thesis is hash rate growth and Bitcoin accumulation, OMN gives you that exposure with the equity-specific noise stripped out. If your thesis is one operator outrunning the rest, you still need the equity. Most allocators serious about this sector will probably end up holding both, sized differently than they were a year ago.

BTW, a few more notes if you are interested in OMN: you'll need a whitelisted wallet to hold it, and secondary liquidity will look like every other tokenized institutional product in this category. Expect it to be thin in the early days. Always check rules about lock-ups & redemption mechanics are other details.

And if you’ve already looked at OMN or sized a position, reply to this email. I’d like to hear how you’re thinking about it against your existing miner book.

Disclaimer: This content is for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities. The Omnes Mining Note (OMN, Series 1) is offered by private placement only, exclusively to non-US persons qualifying as professional investors under MiFID II.