I have to admit that the topic of SpaceX's IPO is impossible to avoid at this point of time. The order book closed roughly four times oversubscribed at a $1.75 trillion valuation, which is peak FOMO by any definition. Yet at the same time, risk assets everywhere else have been getting hit. Crypto had one of its ugliest weeks of the year, and megacap tech hasn't been spared either.

FOMO on one side, bear market on the other. That didn't make sense to me, so I spent a few days trying to understand this IPO properly. The short answer: the two aren't in conflict. The selling is what's funding the FOMO. Once you see how the money moves, the rest of 2026 becomes easier to read, including for the AI-infra and mining names we follow here.

Basics

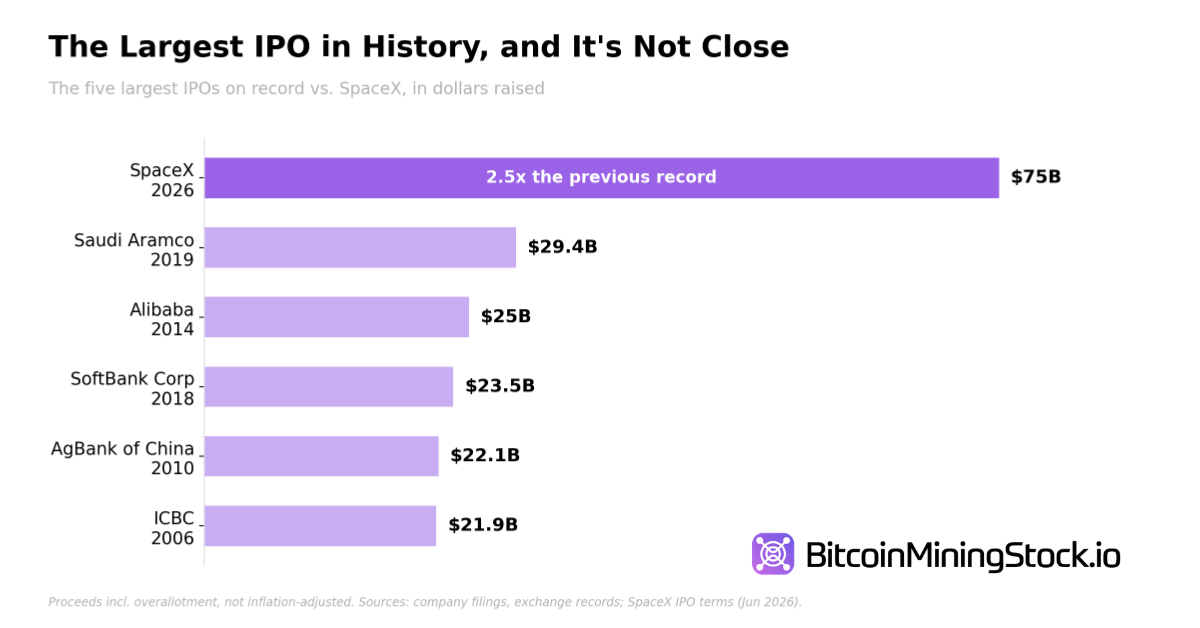

The basics first. SpaceX (SPCX) will list on Nasdaq June 12, selling shares at a fixed $135 to raise about $75 billion at a $1.75 trillion valuation. That's more than double Saudi Aramco's record 2019 raise, and it instantly puts SpaceX among the ten most valuable U.S.-listed companies.

Reported demand reached roughly $250 billion, about four times the shares available. Some institutions put in $10 billion orders on their own. Retail investors also got an unusually large slice: about 30% of the offering through Robinhood, Fidelity, Schwab, SoFi and E*Trade, when big IPOs typically reserve 5-10% for them.

Which raises the question nobody in the FOMO crowd seems to care: where does $250 billion of IPO demand come from?

Someone Has to Sell First

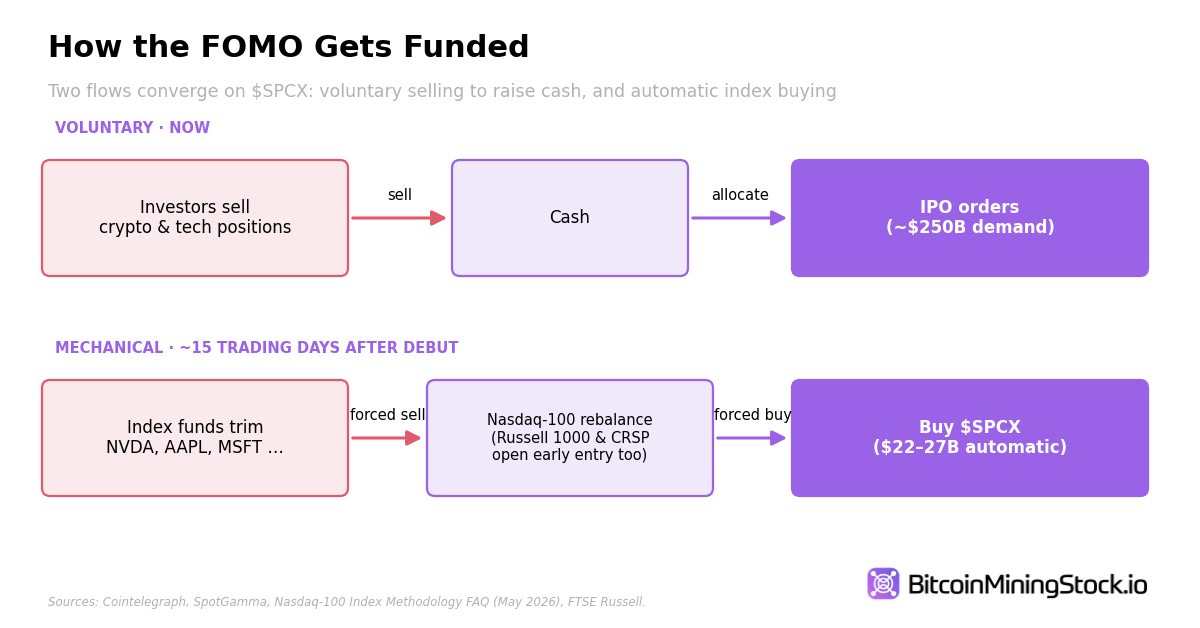

Nobody keeps that kind of money in cash. To fund an allocation, investors sell what they already own, usually liquid positions with gains to take. Multiply that across thousands of accounts chasing the same deal in the same week, and capital gets pulled out of everything else.

That's the bridge between the two moods. Crypto lost over $180 billion in value the same week the order book filled up, and one research desk called it an "IPO tax" on the rest of the market. I'd be careful with that label, since rate-cut doubts and leveraged liquidations were doing damage too. No single deal explains a drawdown that broad. But the basic flow is hard to argue with: when the largest IPO in history closes its books, the cash comes from somewhere, and "somewhere" means whatever investors can sell quickly.

The FOMO and the bear market are the same trade, seen from opposite ends.

Index Funds Become Buyers

Here's what makes this IPO different from every other big listing: part of the buying isn't even voluntary.

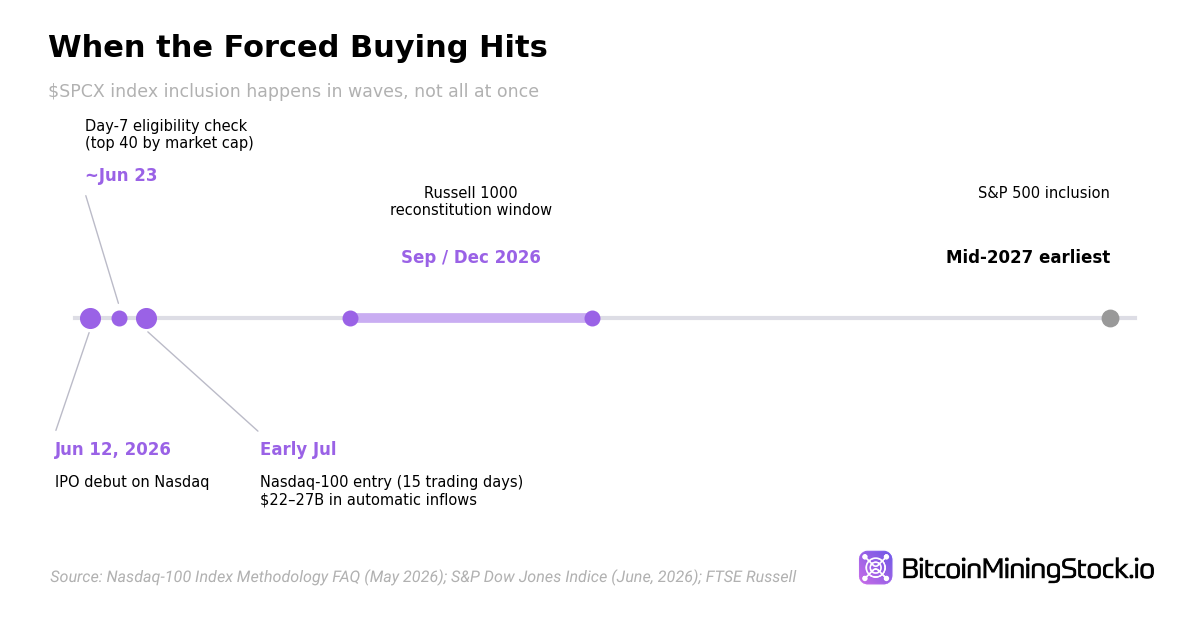

Nasdaq changed its index rules this spring, clearly with SpaceX in mind. A new listing that ranks in the top 40 by market cap can now join the Nasdaq-100 just 15 trading days after its debut. The old three-month waiting period is gone, and the minimum float requirement was scrapped entirely. FTSE Russell loosened its float rules too. Only S&P Dow Jones refused to follow: on June 4 it rejected its own fast-track proposal, which keeps SpaceX out of the S&P 500 until at least mid-2027.

In practice, this means that within about three weeks of listing, every fund tracking the Nasdaq-100 will buy SpaceX. Estimates put that automatic buying at $22-27 billion. And since index funds are always fully invested, they have to sell a little of everything else to make room. Nvidia, Apple, Microsoft, Amazon, and the AI-infra names that have made it into the Nasdaq-100 all get trimmed to fund the purchase of SPCX.

So if you hold QQQ or any Nasdaq-tracking fund in your retirement account, you're in this trade whether you chose it or not. S&P 500 fund holders are spared for now. Their wave of forced buying got pushed to 2027.

Then the Insiders Arrive

One more detail matters before the debut: only 3-5% of SpaceX's shares will actually trade at first. Squeeze $22-27 billion of automatic index buying, plus traders front-running it, in combination with an oversubscribed retail base into a float that small, the early price action will almost certainly look spectacular.

But supply is coming, and on an unusually fast schedule. Instead of the standard 180-day lockup, SpaceX negotiated a rolling one. Insiders can sell up to 20% of their holdings just two days after the first earnings report, with more unlocking through the fall. Musk and a few major backers accepted a full one-year lockup, but they're the exception. The early money, investors who waited a decade for this exit, gets their first window within weeks.

Tesla's S&P 500 inclusion in December 2020 is the template. The stock ran about 70% into the inclusion date, then drifted sideways and down for weeks once the forced buying ran out and the front-runners rotated elsewhere. SpaceX is the same event with a smaller float and a faster clock.

Why This Matters for Our Corner of the Market

So why write about a rocket company on a platform that covers miners and AI infrastructure? Because it's not a one-off and will happen again.

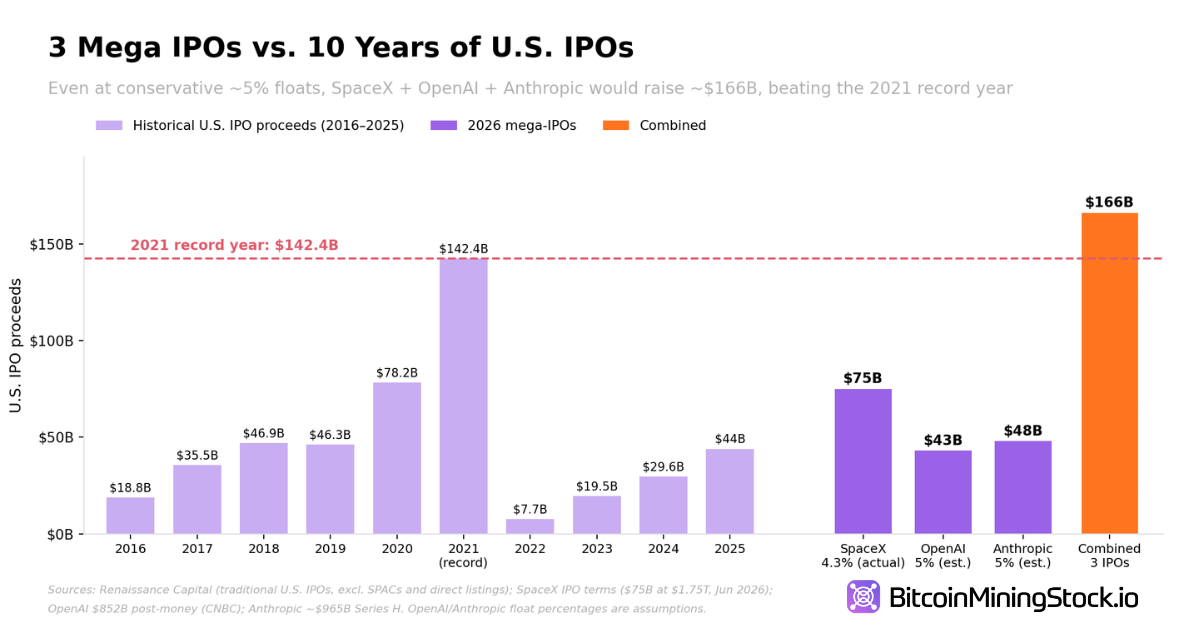

Anthropic filed confidentially for an IPO on June 1. OpenAI followed a week later, and its CFO has hinted at a listing as soon as Q4. If both happen, we get the three largest IPOs in history inside about six months, each one pulling tens of billions out of existing positions, each one repeating the same index mechanics and the same liquidity tax.

For the names we cover, that cuts two ways. The sector runs on outside capital. Every HPC buildout we've analyzed this year was funded by convertible notes, equity raises, or debt, and those deals price off market conditions. A market that keeps getting drained to feed mega-IPOs is a market where financing costs more and windows close faster. On the other hand, the money exiting SpaceX after the inclusion pop has to land somewhere, and AI infrastructure is the obvious nearby trade. Volatility in both directions, in other words.

Final Thoughts

After all the digging, my read is simple. This is not a story about space, and it's only partly a story about SpaceX. There's a huge amount of money being rearranged at a pace the market hasn't absorbed before, with two more rearrangements already lined up behind it.

My prediction: the market stays shaky and choppier than headlines suggest through the summer, and any calm before the OpenAI and Anthropic listings should be treated as temporary. The SPCX debut itself will probably dazzle. A tiny float plus forced buying makes that nearly automatic. But the Tesla 2020 playbook rewarded patience, not buying the top.

If you're sitting on cash and itching to get in right now, I'd be cautious. The forced buying needs time to run its course, the insider supply hasn't hit yet, and better entries usually show up after events like this, not before them.

Disclaimer: The views expressed in this article are my own and are based on publicly available information. This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results. No recommendation or advice is being provided as to the suitability of any investment for any particular investor.